Stabilization at a moderate pace (Martin Ertl)

4 weitere Bilder(mit historischen Bildtexten)

German Industrial Production by Goods

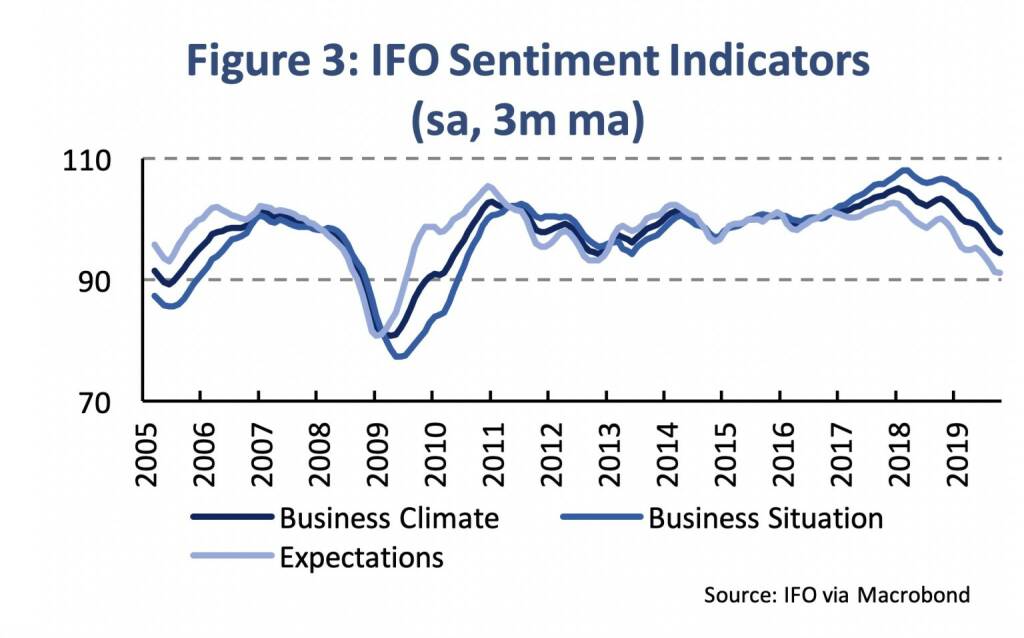

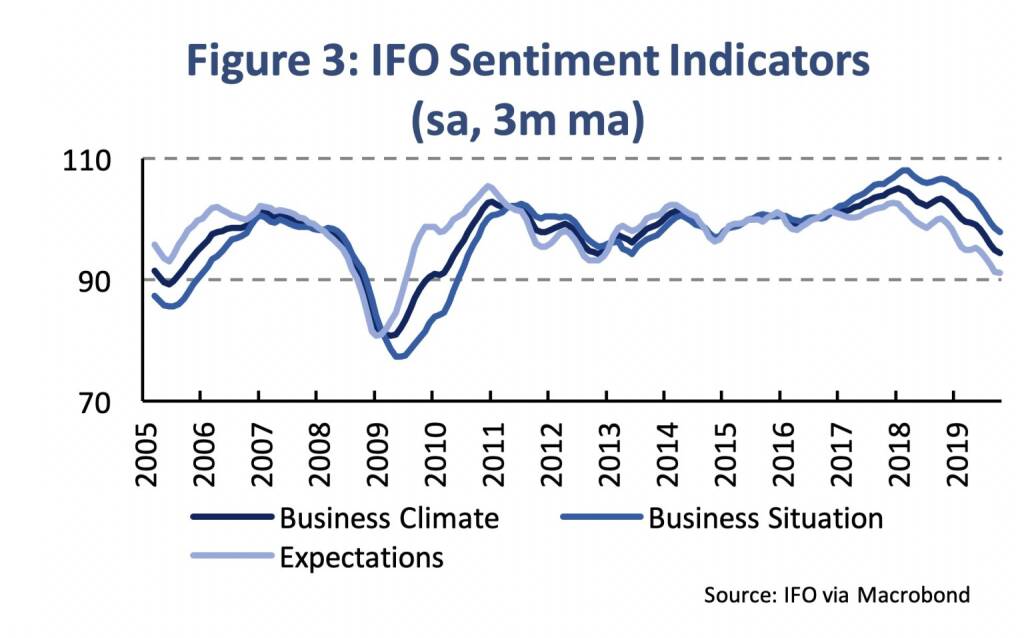

IFO Sentiment Indicators

GDP Growth in Q3

Interest Rate Projections

Ryuji Miyamoto

Ryuji Miyamoto Harry Gruyaert

Harry Gruyaert JH Engström

JH Engström João Linneu

João Linneu19.11.2019, 4743 Zeichen

- Business and sentiment indicators have stabilized at low levels, a turning point has not yet been fully confirmed by the data.

- The German economy has avoided a technical recession in Q3 with 0.1 % GDP growth. Manufacturing industries remain in contraction.

- Growth in CEE countries continues to be above the EU average, being particularly strong in Poland and Hungary.

During the third quarter, the Euro Area economy has avoided a further deterioration in economic momentum. GDP growth has been confirmed at 0.2 % (quarter-on-quarter, seasonally adjusted), which is unchanged to the previous quarter. Further, the expected technical recession in Germany (two consecutive quarters of negative q/q GDP growth) has not materialized. The pace of economic expansion seems to have stabilized for now at a moderate, though, positive level.

The German economy, which has fallen from a growth leader to a growth laggard, has expanded by 0.1 % (q/q) in Q3. A recession has been avoided, yet GDP growth in Q2 had to be revised downwards to -0,2 % from previosuly -0,1 %. So far, we only have suggestive evidence regarding the particular drivers of growth in Q3, as details have not yet been released. Destatis, the German Federal Statistical Office, indicated that private consumption, government consumption, net exports and residential investment had a positive effect on economic growth. Non-residential investment, however, further declined. This account is broadly consistent with short-term business cycle indicators (figure 1). Industrial production (-1.1 %, q/q) continued its decline, while retail sales (0.6 %) as well as exports (0.7 %) stepped up compared to the previous quarter.

The manufacturing sector has been the Euro Area’s problem child for some time, while the service sector prevented a more severe deterioration in the economy. From the high in August 2018, Euro Area industrial production has declined by 3 % until July 2019, since when a very moderate improvement has occured (0.5 %). As expected, the decline had been most pronounced for capital goods and least for consumer goods. German industry data show that it might be too early for a turning point to be identified. German industrial production again contracted in September (-1 %, m/m, excl. construction), reaching the lowest level since November 2015. On a three month moving average basis, industrial momentum has improved somewhat lately, yet growth rates remains in negative territory. Irrespective of the type of goods, industrial production remains in contraction (figure 2). The manufacture of pharmaceutical products, electrical equipment and motor vehicles continue to be most exposed. However, the strugge in the German manufacturing sector remains broadbased, as more than half of industries are in decline.

Business sentiment indicators, which tend to lead the business cycle, have stabilized in recent months. German business climate, as measured by the IFO index, has reached a low in August at 94, which is the lowest level since 2012, and has remained quite stable since then (94.6 in October, figure 3). Sentiment indicators, therefore, do not indicate a turning point, thouhg confirm a stabilization at the current moderate pace. Expectations with regard to business development in the next six months have not stepped up either. It was only during the Financial Crisis of 2008/09 that German businesses had a grimmer outlook regarding the near future. Next week’s release of IFO business sentiment indicators for November may already signal a brighter outlook.

Among Euro Area and European Union member states, all economies expanded during the third quarter (figure 4). Besides Germany, also Austria and Italy reported slow growth momentum at 0.1 % (q/q GDP growth, sa). The fastest growing EU member states can be found in CEE. Poland and Hungary, in particular, experienced strong quarter-on-quarter GDP growth at above 1 % (PL: 1.3 %, HU: 1.1 %). The resilience against the German business cycle slowdown, thus, remains surprisingly strong. Our nowcasting tool has predicted a more moderate expansion in Poland, based on weaker industrial production and stagnating construction and retail sales. Potential downward revisions should, therefore, not be ruled out. In the Czech Republic and Slovakia, growth momentum slowed to 0.3 % (CZ) and 0.4 % (SK). Details about the structure of growth will only become available in early December, though, it has been indicated that both domestic and external demand contributed to GDP growth, at least in the Czech Republic. Growth momentum in CEE countries continues to remain above the EU average.

Authors

Martin Ertl Franz Xaver Zobl

Chief Economist Economist

UNIQA Capital Markets GmbH UNIQA Capital Markets GmbH

Wiener Börse Party #1211: ATX fester, starke Andritz überholt Do&Co (war mehr als 1100 Tage vorne) in unserer 25-Jahres-Wertung

Bildnachweis

1.

German business cycle indicators & GDP growth

2.

German Industrial Production by Goods

3.

IFO Sentiment Indicators

4.

GDP Growth in Q3

5.

Interest Rate Projections

Aktien auf dem Radar:Rosenbauer, Kapsch TrafficCom, Palfinger, Austriacard Holdings AG, Semperit, CPI Europe AG, VIG, FACC, Emerald Horizon AG, Lenzing, Gurktaler AG VZ, Marinomed Biotech, Rath AG, Verbund, Wolford, Wolftank-Adisa, BKS Bank Stamm, Amag, DO&CO, EuroTeleSites AG, Österreichische Post, Telekom Austria, UBM.

Random Partner

Raiffeisen Zertifikate

Raiffeisen Zertifikate ist der führende österreichische Anbieter, der mit über 5.000 Anlage- und Hebelprodukten seit mehr als 20 Jahren in der DACH-Region genauso wie in vielen Märkten Zentral- und Osteuropas zu Hause ist. Einfach kompetent und schnell Marktentwicklungen handelbar zu machen, dafür steht Raiffeisen Zertifikate - Egal ob auf Aktien, Aktien-Indizes, Rohstoffe oder einzelne Themen basierend. Raiffeisen Zertifikate ist eine Marke der Raiffeisen Bank International AG.

>> Besuchen Sie 55 weitere Partner auf boerse-social.com/partner

Latest Blogs

» Österreich-Depots: Zum Ultimo stärker (Depot Kommentar)

» Börsegeschichte 31.7.: AT&S, CA Immo, Strabag (Börse Geschichte) (BörseG...

» Nachlese: Indexzertifikate der Imaps Capital von Andreas Wölfl, Christia...

» PIR-News zu RBI, Bawag, Kontron, WEB Windenergie, Addiko, Research zu Ve...

» Andritz überholt Do&Co: Wechsel an der Spitze der Wiener 25-Jahres-Wertu...

» Wiener Börse Party #1211: ATX fester, starke Andritz überholt Do&Co (war...

» Wiener Börse zu Mittag fester: Verbund, VIG und AT&S gesucht

» Österreich-Depots: Etwas schwächer (Depot Kommentar)

» Börsegeschichte 30.7.: Extremes zu Porr (Börse Geschichte) (BörseGeschic...

» Nachlese: Vor Österreich-Tag bei der Deutsche Börse, Catharina Ahmadi (...

Useletter

Die Useletter "Morning Xpresso" und "Evening Xtrakt" heben sich deutlich von den gängigen Newslettern ab.

Beispiele ansehen bzw. kostenfrei anmelden. Wichtige Börse-Infos garantiert.

Newsletter abonnieren

Runplugged

Infos über neue Financial Literacy Audio Files für die Runplugged App

(kostenfrei downloaden über http://runplugged.com/spreadit)

per Newsletter erhalten

- Wiener Börse: ATX am Freitag kaum verändert

- Wiener Börse Nebenwerte-Blick: Marinomed steigt 8...

- Wie Rath AG, Wolftank-Adisa, Marinomed Biotech, R...

- Wie Verbund, Palfinger, AT&S, RBI, VIG und Porr f...

- Neue Kursziele für Andritz und Verbund

- Österreich-Depots: Zum Ultimo stärker (Depot Komm...

Featured Partner Video

Books from Friends #5: Horst Skoff - Mehr als ein Rockstar (Gernot Fleiss-Cianciabella)

Mein Buch "Ein Fanboy über die jüngere Geschichte der Wiener Börse im Remix mit Sport, Musik und (m)einer Biografie" ist erschienen, alle Infos unter christian-drastil.com. Im Buch spielt die Zahl ...

Books josefchladek.com

Wij zijn 17

1955

C.A.J. van Dishoeck

Achter Glas

1957

C. de Boer jr.

Formes nues

Formes nues Mark Mahaney

Mark Mahaney Karl Blossfeldt

Karl Blossfeldt